Uelzena’s topics for the future

Economy, society, environment - there is a wide range of possible topics regarding corporate sustainability. The Uelzena Group continually analyses in a proven procedure which topics are essential for the organisation and its stakeholders. In 2018, this process was further developed.

Each company has to define their own relevant topics. Experts call this procedure in which the company selects their sustainability topics and weights them according to significance (principle of materiality) “materiality analysis”. It is a proven process that has been used by numerous companies worldwide. Each company can then define for itself on how the procedure is to be carried out in detail. One important requirement: It must follow plausible rules.

The Uelzena Group and the world

It was as early as 2014 when the Uelzena Group conducted its first materiality analysis, which included both its own views and the views of external and internal stakeholders. The result was a list of 20 topics. In 2018, we repeated the materiality analysis but revised the procedure used.

Companies are not closed systems - disconnected from the rest of the world. On the contrary: They are more or less connected with their environment. Thus the basic goal of our materiality analysis was to investigate the corresponding interaction.

There are many questions relating to materiality analysis

Uelzena eG analysed the impact of the economy, society and ecosystems on the organisation. It was therefore necessary to identify issues that are important for the Uelzena Group and its long-term success as an economic cooperative. On a global level, for example, this could be the growing global demand for dairy products, or regionally the construction of a highway that better links the locations and facilitates the search for skilled workers.

At the same time, the company wanted to explore the – positive and negative – impact it has on the environment. This required asking questions such as: How significant is the Uelzena Group as an employer and how does it factor in the economy at the respective locations? How high and relevant are the CO2 emissions of the Uelzena Group?

The fundamental basis: a three-part analysis

In order to do justice to this comprehensive thirst for knowledge, the Group has broadly laid out its materiality analysis. It comprises several parts:

- An external environment analysis that identifies and evaluates relevant factors outside of the company. Included here is the identification of opportunities and risks of future developments.

- An internal corporate analysis, which in particular looks for relevant topics in the profile of the Uelzena Group, its core competencies as well as values, guidelines and management systems. These topics are then compared with relevant competitors and the expectations of the various stakeholder groups and evaluated in order to determine the strengths and weaknesses of the company.

- The analysis of internal and external stakeholders. Relevance of topics from the stakeholders’ point of view, their expectations and requirements.

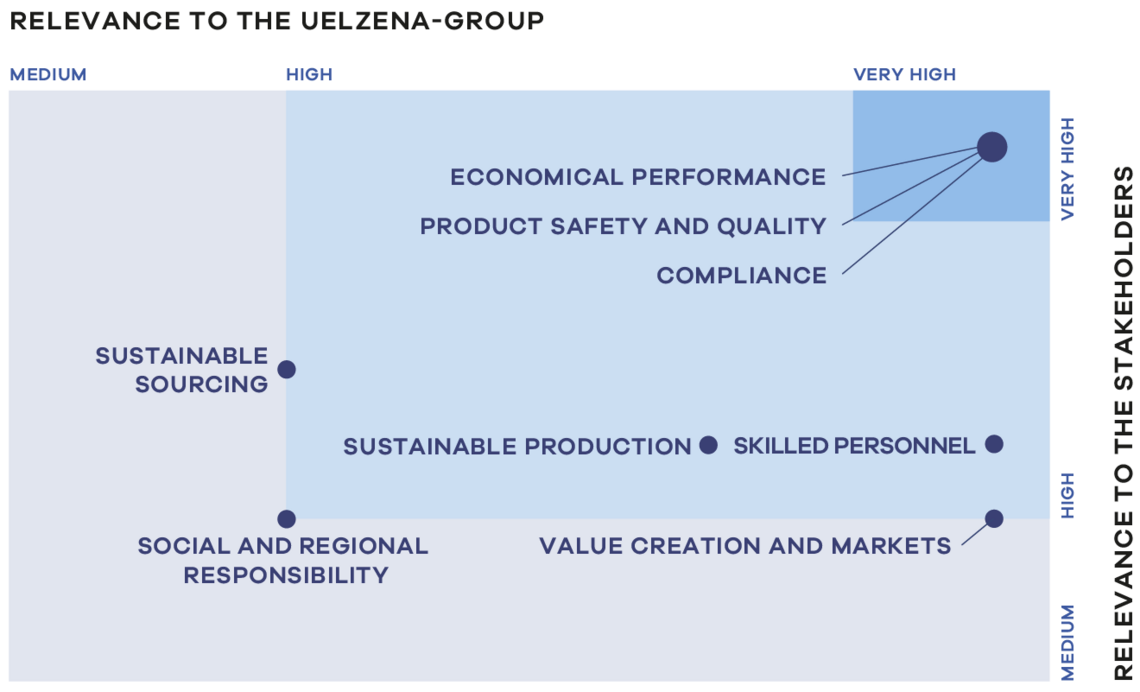

The result of the new materiality analysis can be displayed in a chart with two axes. It shows the significance of topics from both the company and stakeholder’s point of views. The strengths and weaknesses as well as opportunities and risks of the Uelzena Group are summarised in a so-called SWOT analysis for the topics evaluated as essential.

MATERIALITY ANALYSIS: KEY ASPECTS OF THE UELZENA GROUP

The Sustainability Working Group of the Uelzena Group conducted the new materiality analysis 2018 in several workshops. At these meetings, it was established, amongst other things, which geographical and industry-specific framework or context is relevant for our company. This is important in order to be able to define topics and to know where a topic has an effect. In detail: At which location, at which level (local, national, global), inside or outside of our company, at which link in our supply chain or in the industries which are important to us?

This was followed by an extensive collection of possible topics in addition to the aspects already identified in the 2014 materiality analysis. Sources included public discourses, experts, laws, guidelines, international agreements, our corporate key values and strategies, competitors, and industry requirements.

Stakeholders are another source of topics. The stakeholder dialogue within the Uelzena Group is an ongoing process and involves a constant exchange between the company and the stakeholders. For each stakeholder group, a specific employee is responsible for conducting these dialogues and handling the discussion of the respective issues. The responsible employees note down the views of the respective stakeholder group and contribute this knowledge when the Uelzena Group meets internally for workshops and to carry out the materiality analysis.

Similar or closely related topics were then grouped together into topic groups. For each topic group, the Working Group briefly explains why the respective topic has been selected, where it has an impact, how strongly the Uelzena Group is affected by it, and how great the impact is to our company.

From this collection, the most important topics for the Uelzena Group had to be identified. It was also examined whether there are legal or voluntary obligations on a topic and whether a topic is already actively managed, both of which are strong indications and are allocated high relevance. Moreover, a numerical scale is used to indicate the impact extent that a topic has on the business model or reputation of the Uelzena Group and the extent to which the Uelzena Group has an impact on the environment, society and the economy. The judgements of the key stakeholder groups are also included in this assessment.

The result of this materiality analysis is a list of topics sorted by priority, both from the company and the stakeholders' points of view. In the second step, these key topics were allocated according to topic to the five strategic fields of action. For instance, the topics “Product safety and quality”, “Development of value creation and markets” and “Sustainable sourcing” are allocated both from a content and strategic perspective to the action field “Products”. Despite this consolidation, all topics are independent and have different preferences within the organisation and among the stakeholders.

New topics through dialogues

The Uelzena Group is in constant dialogue with its key stakeholders. An employee who systematically records the requirements and expectations is responsible for the exchanges between these particularly important stakeholder groups. In this way, we learn about the concerns and opinions of the representatives of the key stakeholders, particularly with regard to:

- Current expectations and requirements to the Uelzena Group.

- The Uelzena Group’s strengths and weaknesses as seen from the stakeholders’ point of view.

- Evaluation of the current strategy, measures, systems and processes of the Uelzena Group.

- The question regarding what changes the stakeholders feel the company will be facing in the coming years, including those that involve both opportunities and risks.

Details on this orderly procedure and on the results regarding the selection of topics are described on the web page materiality analysis.

THE KEY ASPECTS OF THE UELZENA GROUP

Focus on corporate purpose

Priority: Very important

Field of Action: Company

Sub-topics: Includes milk payout, net income, shareholders' equity, liabilities, changes in the number of employees.

Sustainability context: Significant both inside and outside the company (members, suppliers & service providers, employees, regional/local communities and economy).

Influence/impact: The great importance of the Uelzena Group as an employer and value-adding factor in structurally weak regions around their sites. Central importance of economic performance for the ongoing viability of the Uelzena Group as an independent economic player.

Safety is a basic requirement

Priority: Very important

Field of Action: Products

Sub-topics: Includes audits, continuous improvements, documentation and information of the food industry, labelling of products, quality management with hygiene and allergen concepts, traceability, internal inspections.

Sustainability context: Significant both inside and outside the company (suppliers, customers, consumers/society, internal procedures, processes and employees).

Influence/impact: Customers of the Uelzena Group request product quality and product safety along the supply chain. Supplying the society with high-quality and safe food products. Drastic consequences of mistakes that can lead to loss of confidence and damage to health.

Compliance with rules

Priority: Very important

Field of Action: Social and regional responsibility

Sub-topics: Includes compliance with legal regulations, contracts and voluntary commitments (ethics & responsibility).

Sustainability context: Significant both inside and outside the company (suppliers, customers, official authorities, within the company for example, purchasing and production departments).

Influence/impact: Complying with laws, regulations and voluntary commitments, preventing penalties that are damaging to our company and loss of reputation. In addition, compliance with these rules will protect the environment and society.

Securing the future of the company

Priority: Important

Field of Action: Employees

Sub-topics: Includes training and further education, transfer of knowledge, employer branding.

Sustainability context: Significant within the company (employees).

Influence/impact: Demographic change could lead to a shortage of skilled workers in the future. The targeted recruitment and training of skilled workers is a remedy for this impending shortage. A good and future-oriented training and further education program promotes the expertise of employees and prepares them for the loss of work in the course of advancing technical developments.

Focus on customers and performance

Priority: Important

Field of Action: Products

Sub-topics: Includes corporate strategy, focus on growing market segments, differentiation strategy, appropriate investments in production and marketing, risk management through diversification, transparency and measurability.

Sustainability context: Significant both inside and outside the company (production at the Uelzena sites, members, suppliers, regional/local communities).

Influence/impact: Successful value creation and focus on growing markets ensuring the company's business success. The more profitable the company is, the better the Uelzena group can fulfil its mission and pay its members competitive milk prices.

Environmental protection in the company

Priority: Important

Field of Action: Production

Field of Action: Products

Sub-topics: Includes energy, climate protection/greenhouse gas emissions, air pollution control, noise exposure, wastewater, waste, consumption of resources.

Sustainability context: Significant both inside and outside the company (production at the Uelzena sites, climate/atmosphere).

Influence/impact: Investments in higher energy efficiency help to save fossil fuels and costs. This improves competitiveness. At the same time, CO2 emissions per product unit (kg) and relative atmospheric pollution with climate-damaging emissions are reduced.

Responsible design of supply chains

Priority: Important

Field of Action: Products

Sub-topics: Includes humane working conditions and environmental and climate impacts on supply chains, animal welfare in raw milk production, proportion of products with recognised seals and sustainability standards.

Sustainability context: Significant outside the company (suppliers of milk, suppliers of non-dairy products such as sugar, cocoa and coffee, dairy farm animals), environment at production sites of milk/sugar (Germany), cocoa/coffee (non-EU countries), agricultural workers on coffee and cocoa plantations.

Influence/impact: The topic is being driven by key customers and society and is becoming increasingly important for business success. By demanding transparency about production conditions from its suppliers, the Uelzena Group has a positive development process.

Our responsibility for the regions around our sites

Priority: Important

Field of Action: Social and regional responsibility

Sub-topics: Regional milk production, regional labour markets, responsibility for regional economic strength, attractiveness of regions around the sites, especially for young people.

Sustainability context: Significant outside the company

Influence/impact: The Uelzena Group is one of the larger industrial enterprises at the respective locations with a relatively large influence on the regional labour market, local supply, small trade companies and service providers. When it comes to infrastructure measures or environmental protection issues, we are important as a discussion partner for authorities. The company and its employees contribute financially and through volunteer work to ensuring that the regions around our sites remain attractive places to live and work.